As I do every month, I send you my warmest regards, having just returned from two weeks in the sweltering heat of Europe, and one day after seeing the dream and hope of watching Mexico’s soccer team join the elite of world soccer dashed. As I mentioned in the letter’s title, bilateral relations are at one of their most critical junctures, with the U.S. attacking Mexico on various fronts: unsubstantiated accusations of illicit financial transactions (Vector, CI, Intercam), governors implicated with the cartels (Rocha Moya), and now the allegations against officials involved in fuel theft. I do not doubt that all of this is true, but there has been no response from Mexico demanding evidence or acting as the aggrieved party; the only expression of defense has been the morning press conferences, which have led nowhere.

The decision not to extend the USMCA for the proposed 16 years and to keep it under annual review is not the end of the world for Mexico. Still, it is another source of pressure that creates uncertainty and limits foreign investors’ ability to make long-term plans to build new factories, given the possibility that the free cross-border flow of their products could be eliminated within a year. President Trump started with Venezuela, moved on to Iran, and it’s rumored he’ll next target Cuba—will Mexico be next? Trump has not visited Mexico during his current administration—a visit that has always underscored the “good neighbor” policy—and while he has said that Sheinbaum is a good person, he has continued to mock her, imitate her speech, and fail to acknowledge the importance of the relationship.

There are 40 million people of Mexican origin in the United States, with significant economic clout (it would be the seventh-largest economy in the world), whose political influence is growing every day, and who should be a positive factor in the bilateral relationship, but both presidents tend to ignore them. I will set this debate aside—one that concerns me greatly—to turn to an analysis of the situation in the United States. President Trump, author of the book *The Art of the Deal*, could write a sequel titled *The Art of Backtracking*, since he repeatedly draws lines in the sand, threatens to attack if Iran dares to cross those lines, and, when push comes to shove, draws new lines without following through on his threats. He has done the same with his tariff policies. The cost of the war with Iran already exceeds $100 billion for the U.S., not including the cost to Israel or the impact on the rest of the world.

It is obvious that Trump has been weakened in the eyes of the world, and even many Republican senators and representatives have turned against him. This is due to inexplicable actions such as the creation of a $1,776 million fund using taxpayer money to compensate participants in the January 6, 2021, march on the Capitol—money that would have come from withdrawing his lawsuit against the IRS for allowing his tax returns from previous years to be released, a lawsuit that was apparently dropped. Other inexplicable actions include renaming the Kennedy Center the Trump Kennedy Center, the attempt to feature his photo on a new $250.00 bill, and reports of the enormous fortune he and his children have amassed during the 18 months of the current administration.

The economy has remained stable despite the ongoing conflict in Iran, and oil prices have already begun to fall from the $137.00 high reached at the start of hostilities to $68.00 today. Unemployment has remained at 4.2%, although only 57,000 jobs were created last month—a figure below analysts’ projections but not cause for concern, as the previous two months were well above expectations. Inflation jumped to 3.8%, but much of this was due to high fuel prices, which are now returning to normal. The new Fed chairman, Kevin Warsh, was very clear in his inaugural speech, stating that he would wait until there was greater clarity in the economic data before taking action. However, he was very explicit that lowering rates in the short term is not viable and that the next move is expected to be upward in the fourth quarter.

The JOLTS report on job openings showed a significant jump, indicating that there is no need to create job incentives; on the other hand, the increase in workers’ hourly earnings was entirely offset by the rise in gas prices, which is a major concern for Trump, since the midterm elections for the 435 House representatives and 35 senators are coming up in November, and the American people vote with their wallets; if they feel their economic situation has deteriorated, they vote for the party not in power.

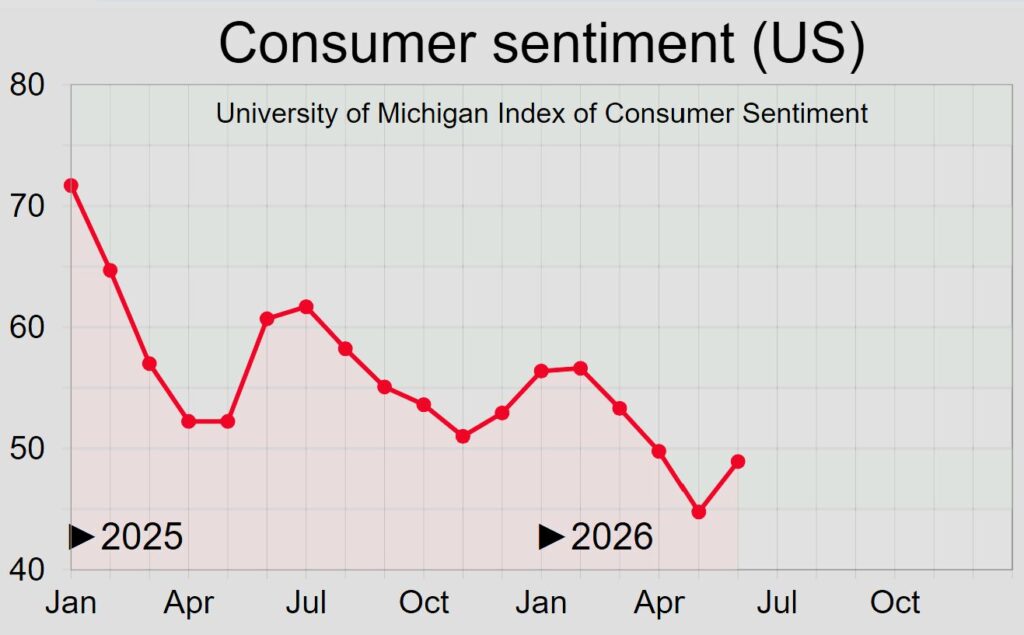

The yield curve has flattened as short-term rates have risen more than long-term rates, indicating that the market expects rate hikes to combat inflation. The Beige Book, which explains the Fed’s decisions, mentions higher inflation and dissent among members regarding keeping rates unchanged rather than raising them. In key economic data, the University of Michigan consumer sentiment index remained above 50, and short-term inflation expectations rose, though they fell by 8 points for the 6-month-plus outlook. The business purchasing managers’ index fell from 51.7 to 51.3 but remains above 50, which is still favorable.

The U.S. Strategic Petroleum Reserve has declined for 10 consecutive weeks and is at its lowest level in 22 years. At the same time, the International Energy Agency reduced its global oil demand forecast from 105 to 104 million barrels per day, with the United States consuming 16 million barrels per day. The productivity report showed a decline from 0.8% to 0.3%, despite a slight reduction in labor costs per unit produced. The construction sector grew by 3.2% from 2025 to 2026, although the average price of homes sold rose by only 0.4%. One factor that impacted the markets and reflects the rise in oil prices is that import prices rose 1.9% over the month and 6.7% over the year, reflecting not only higher costs but also the effect of tariffs.

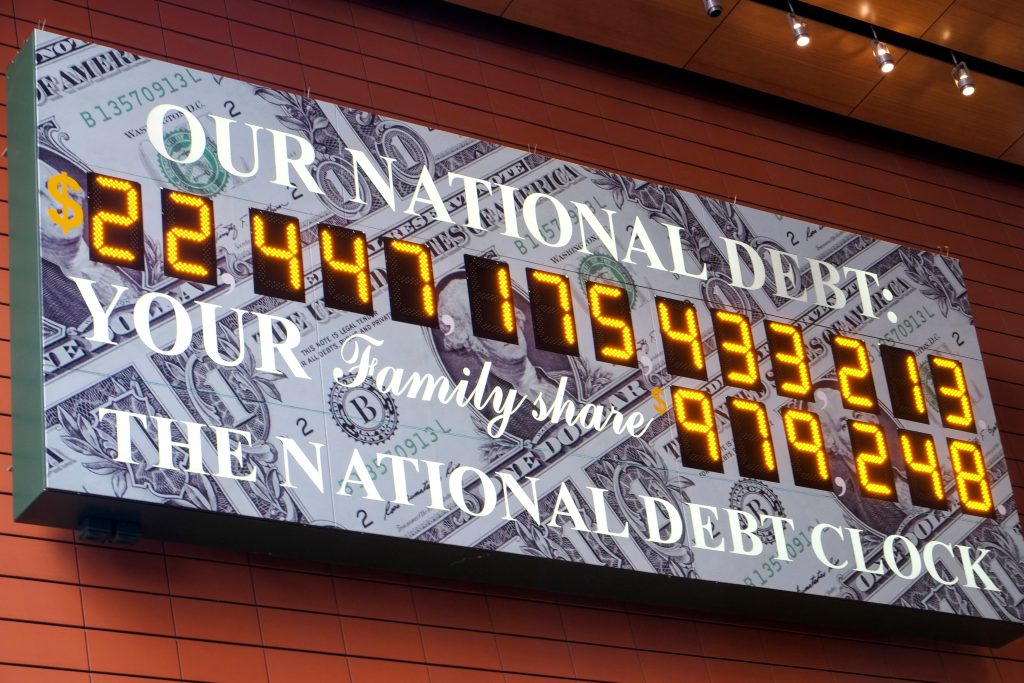

A looming crisis involves the Social Security fund, as it collects 78% of what it pays out and is projected to run out of money in 7 years. Payments will never stop, but the government’s deficit will grow, as will the need to issue even more debt. Speaking of debt issuance in 2026, the government projects issuing $2.1 trillion, the investment-grade private market $1.9 trillion, and the junk bond market $441 billion, which is an enormous amount that will have to be absorbed by investors. A significant portion of this stems from the needs of high-tech companies to finance their growth in artificial intelligence; Google is a prime example, having issued $80 billion in bonds despite generating a fortune in cash flow.

One of the main buyers of government bonds is central banks for their reserves, but these have increased their gold holdings from 20% to 27% of the total, reducing U.S. Treasury bonds from 25% to 22%. Incidentally, many states are restricting the establishment of AI data centers due to their impact on energy costs, having halted $130 billion in investment. AI companies have leased 1 million square feet of office space in New York City, which has become the heart of artificial intelligence. The total market capitalization of U.S. stock exchanges reached $73.7 trillion (excluding Anthropic and OpenAI), 2.38 times the GDP ($3.37 trillion). It exceeded the combined total of the next 10 largest markets worldwide. 30% of the total is accounted for by the value of a new group of six stocks, known as MANGOS: META (Facebook), ANTHROPIC (not yet public), NVDA, GOOGLE, OPEN AI (not yet public), and SpaceX.

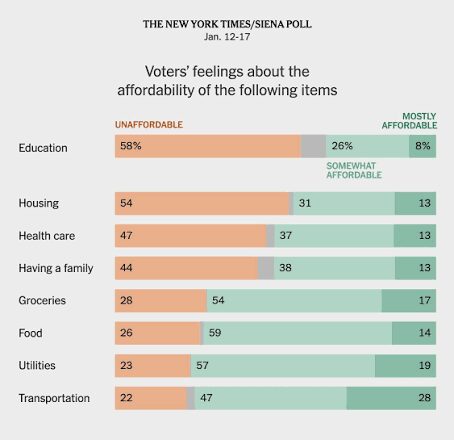

To conclude the discussion on the United States, a large NYT survey found that 40% of middle- and upper-class people feel they do not have sufficient resources to retire comfortably, and 61% believe their children’s future will be more financially challenging than what they have experienced. Analyzing the U.S. economy, the sectoral breakdown of GDP shows that the financial and real estate sector accounts for 21.8% of the total, professional services 13.1%, manufacturing 9.4%, government 11.1%, education and health care 8.9%, wholesale and retail trade 12.6%, and all other sectors 23.1%.

Mexico is returning to reality after the World Cup. It faces the same problems: strained relations with the United States, insecurity, and the lack of an independent judiciary that inspires confidence in citizens. Economic growth remains positive but very low, and the currency’s strength continues to be a boon for importers but a burden for exporters and the tourism sector. The cabinet reshuffle is merely more of the same, and López Obrador’s partial return to the spotlight—along with his son’s departure from MORENA’s leadership—casts some doubt on who is actually leading the country. Meanwhile, business leaders seem unfazed, as business continues as usual, and 135 million consumers represent a formidable force.

As we do every month, we’ve listed some of the positive and negative developments in Mexico.

Positives

· The government plans to boost the petrochemical and fertilizer sectors by $93B.

· Mercado Libre will invest $4.6B this year and $14.2B over the next 6 years, creating 42,000 jobs.

· CFE received 80 partnership proposals and accepted 37 of them despite the 54%/46% government/private sector law, awarding contracts worth $7,411M.

· PEMEX’s losses fell by 30% due to increased production and improved refining.

· Inflation fell to 3.9%, within BANXICO’s target range of 3% + 1%.

· Mexico expects to increase its renewable energy generation from 28.6% to 45% by 2030.

· The second quarter was the best for construction and manufacturing in the last 5 years.

· The World Bank forecasts 1.3% growth, although the IMEF says it will be 1%.

· ANTAD reported that its members increased sales by 0.8% in May, marking 15 consecutive months of growth.

· It finally appears that oil extraction via fracking will be authorized.

· Volaris saw a 7.2% increase in passenger traffic in May.

Negatives

· The most significant negative is the failure to approve the USMCA, although it won’t have much of an impact in the short term.

· IMEF reported that the manufacturing and services indices fell in May.

· Tensions with the United States are rising following the revocation of the visas of Governors Américo Villarreal and Alfonso Durazo.

· Net investment has fallen for 18 consecutive months.

· Consumer confidence stands at 43.5, the lowest figure in 41 months.

· Automobile production fell 3.7%, marking the second-worst year in the last 17 years.

· The economic impact of the World Cup was only $1.08B.

· Carlos Slim, already a major player in the energy sector, stated that it is madness to venture into deep-sea oil extraction, that he will no longer invest in it, but that he believes there will be many interested foreign investors.

Israel saw a slight recovery in June, and the Central Bank revised its GDP forecast upward to 4%, with an even higher increase of 5.5% projected for 2027, despite the IMF lowering its estimate to 3.5% for this year due to the 3.8% contraction in the first quarter. The Central Bank cut the discount rate for the third time this year to 3.5%, the lowest level since 2022, as inflation remained at 1.9%. The government deficit is projected at 4.9% of GDP in 2026 due to massive military spending on the conflict in Iran and the ongoing struggle with Hamas and Hezbollah. The shekel stood at 3 to 1 against the dollar, falling slightly over the month.

In news from the rest of the world, retail sales in China are at their lowest level since the COVID pandemic. Electric vehicle exports reached 209,000 units, driven by the global rise in gasoline prices; inflation stood at just 1.2% on an annualized basis; and a national AI center was announced, with an investment of $295 billion.

In Japan, SoftBank surpassed Toyota as the country’s largest company.

In Europe, Switzerland held a referendum to cap total population growth at 10 million—the current population is 9.2 million—but the measure was defeated at the polls. In Switzerland, 1 in 3 residents is a foreigner, compared to 1 in 6 in the United States.

The European Central Bank raised interest rates by ¼% to combat inflation.

In the Middle East, the United Arab Emirates is moving to eliminate 100% of its oil shipments through the Strait of Hormuz, and Saudi Arabia hopes to achieve the same by mid next year.

In South America, the shift to the right continues, with victories for non-socialist candidates in Peru, Chile, and Colombia—a clear indication that the progressive left is not working and is fueling a wave of citizen protests.

Argentina brought its annual inflation rate down to 33%, and its bonds reached their highest level since Milei took office. Exports grew by 192.3% compared to the previous year, and despite all the good news, the October elections are expected to be very close, as the left remains strong.

Brazil, the strongest country in the region, is facing a serious conflict with the United States, which imposed blanket 25% tariffs on Brazilian goods for “unfair trade.” Exports to the U.S. are at their lowest level since 1997. The Central Bank lowered the discount rate to 14.25%, even though inflation remains at 4.8%, above the 4% limit it had set. The New York-based equity fund that invests exclusively in Brazil experienced its largest outflow of funds since its inception.

Stock markets remain volatile; although the overall trend is positive, bonds are yielding 0.25%, currencies are showing some weakness against the dollar, gold fell below $4,000/oz—though it closed slightly higher—and bitcoin dropped to $58,700 before rebounding slightly above $60,000.

Further Reading: